Disposal Of Rpc Shares In Malaysia

What Is Real Property Gains Tax The Star

Chapter 9

Chapter 9

Transfer Of Shares In A Real Property Company Donovan Ho

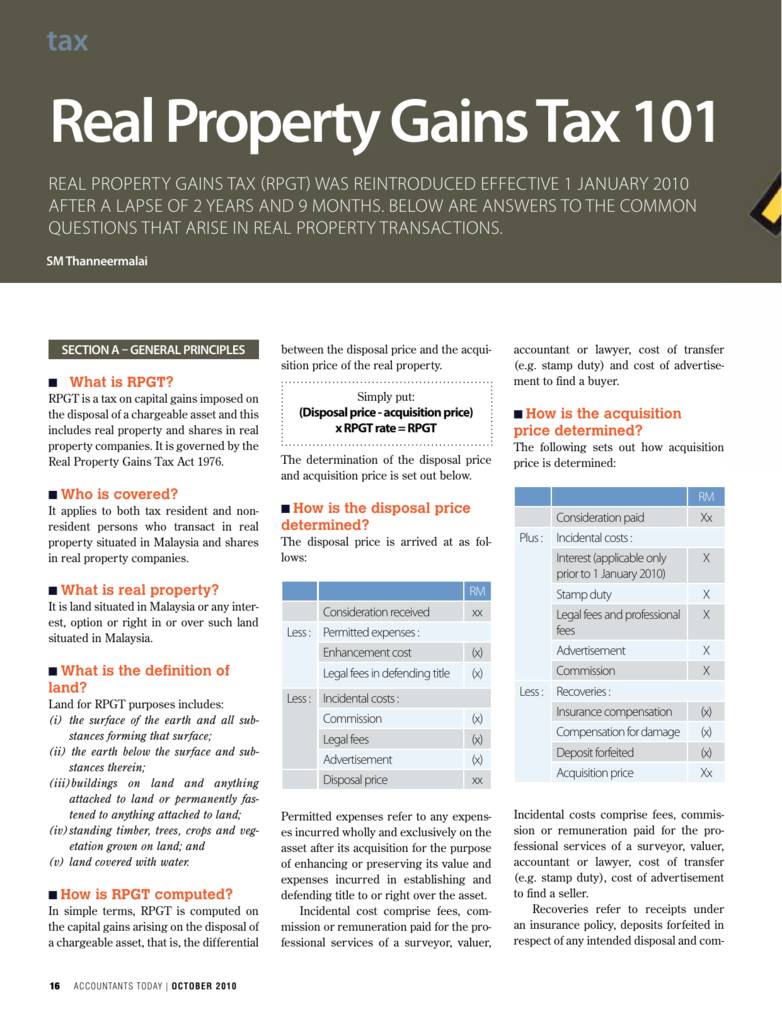

Real Property Gains Tax 101

Real Property Gains Tax Rpgt In Malaysia

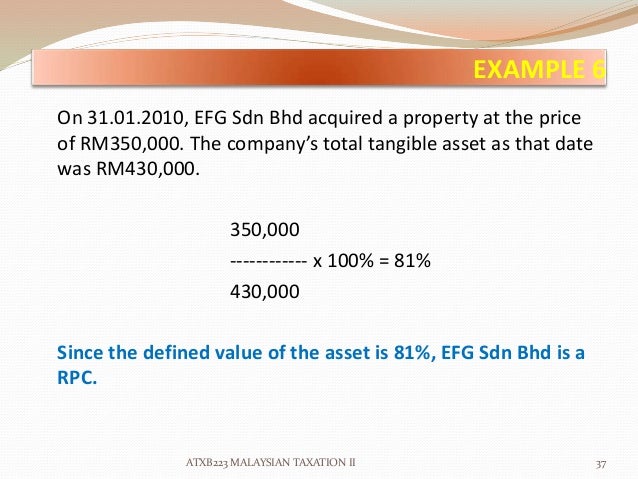

Disposal or acquisition of the rpc shares.

Disposal of rpc shares in malaysia. An rpc is a company holding real property or shares in another rpc with value not less than 75 of the value of the company s total tangible assets. Rpgt is also charged on the disposal of shares in a real property company rpc. Although capital gains are generally not taxed in malaysia one exception to this is the gains arising from the disposal of either real property or shares in a real property company rpc. On gains arising from the disposal of real property situated in malaysia or shares in a real property company rpc.

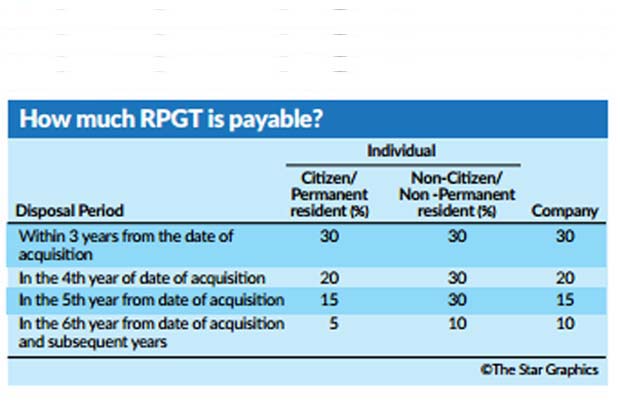

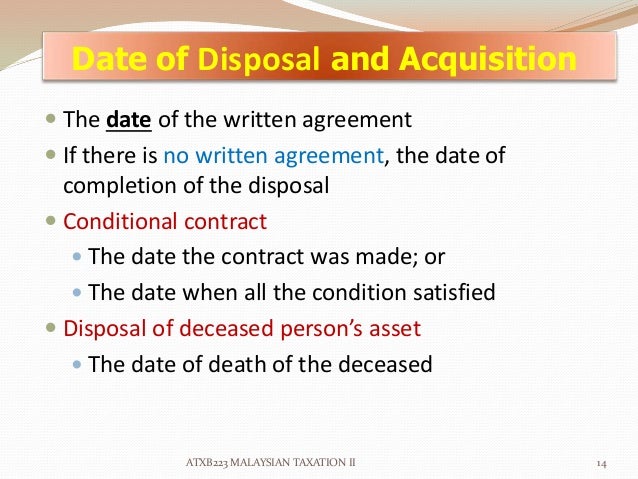

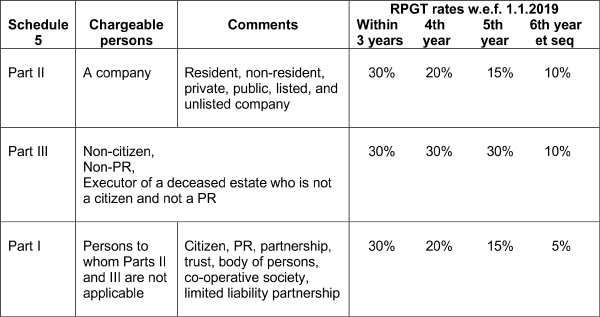

Real property gains tax rpgt is charged on gains arising from the disposal of real property situated in malaysia or of interest options or other rights in a property as well as the disposal of shares in real property companies rpc. Shares in rpc before 1 april 2007 ckht 1 ckht 1 ckht 2 ckht 2 submit the rpgt form within 60 days from the date of disposal to the lhdnm branch which handles the disposer s tax file attach the following documents copy of sale and purchase agreement s p for the acquisition and. Depending on the period of ownership these gains will be subject to rpgt at rates ranging from 30 to 5. Shares in rpc or both whereby the market value of.

There is no capital gains tax regime except for real property gains tax which is applicable to gains on the disposal of real property or shares in real property companies. Rpgt had undergone a couple of revisions since introduced in 1976 and the last revision was done in 2014. Therefore the disposal of such shares will be subjected to rpgt. In some cases the disposal price of the rpc share may also be deemed to be the market value of the rpc shares 10 acquiring an rpc under the rpgt act both the seller and purchaser of shares in an rpc are required to fi le rpgt returns within 60 days from the date of disposal of the shares.

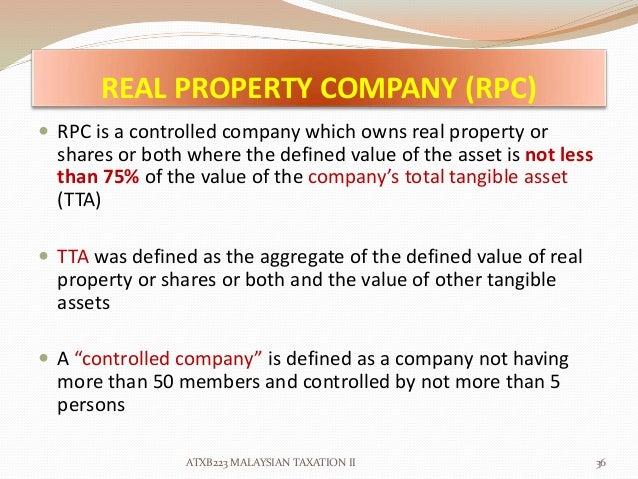

A rpc is a controlled company the major assets of which consist substantially of real property or rpc shares. Malaysia supports the beps initiative and is committed to review and update the local tax legislation to ensure. Under the real property gains tax act 1976 rpgt act an rpc is a controlled company which the defined value of its real property or shares in another rpc or both is at. A rpc is a controlled company holding real property or shares in another rpc as a major asset which is defined as valued more than 75 of the value of its total tangible assets.

Rpgt is charged on gains arising from the disposal sale of real properties or shares in real property companies rpc. Shares in rpc acquirer buyer i. An rpc is a company that owns real property in malaysia or shares in other rpcs to the extent the value of its real property or shares in other rpcs or both is 75 percent or more of the total tangible asset value of the company at the relevant time.

Chapter 9

Chapter 9

Https Www Accaglobal Com Content Dam Acca Global Pdf Students 2012s Sa Apr11 P6mys Rpgt 2 Pdf

Taxation On Properties Rpgt Company Shares Mypf My

Real Property Gains Tax Part 1 Acca Global

Chapter 9

What Is Real Property Gains Tax Rpgt In Malaysia How To

Chapter 9

Http Www Hasil Gov My Pdf Pdfam Risalah R13 Bi 15 Pdf

Understanding Rpgt 2 Real Property Companies Legally Malaysians

Part 1 Rpgt Joint Venture Inheritance Tax

Real Property Gains Tax Part 1 Acca Global

Chapter 9